The Economics of Early Cancer Detection

Major diagnostics companies are investing billions into multi-cancer screening tests. But will it be a profitable market?

Multi-cancer early detection tests - simple blood tests that can detect cancer in its earliest stages, while it’s most treatable - are an obviously charismatic idea. So much so that one of the pioneering companies in the space, GRAIL, chose its name to evoke the “holy grail” of medicine.

In development for a decade, “MCED” tests are marching forward steadily, spurred on by heavy investment from both major diagnostics companies (Guardant, Natera, Exact) as well as smaller challengers (GRAIL, Freenome, DELFI Diagnostics).

MCED tests are far from perfect: accuracy varies widely across cancer types and stages. Despite this, I expect them to gain clinical adoption in the next several years. Will this be a market that generates significant profits? Here, I’ll review the science behind MCEDs, and evaluate their economics in depth.

The MCED Opportunity

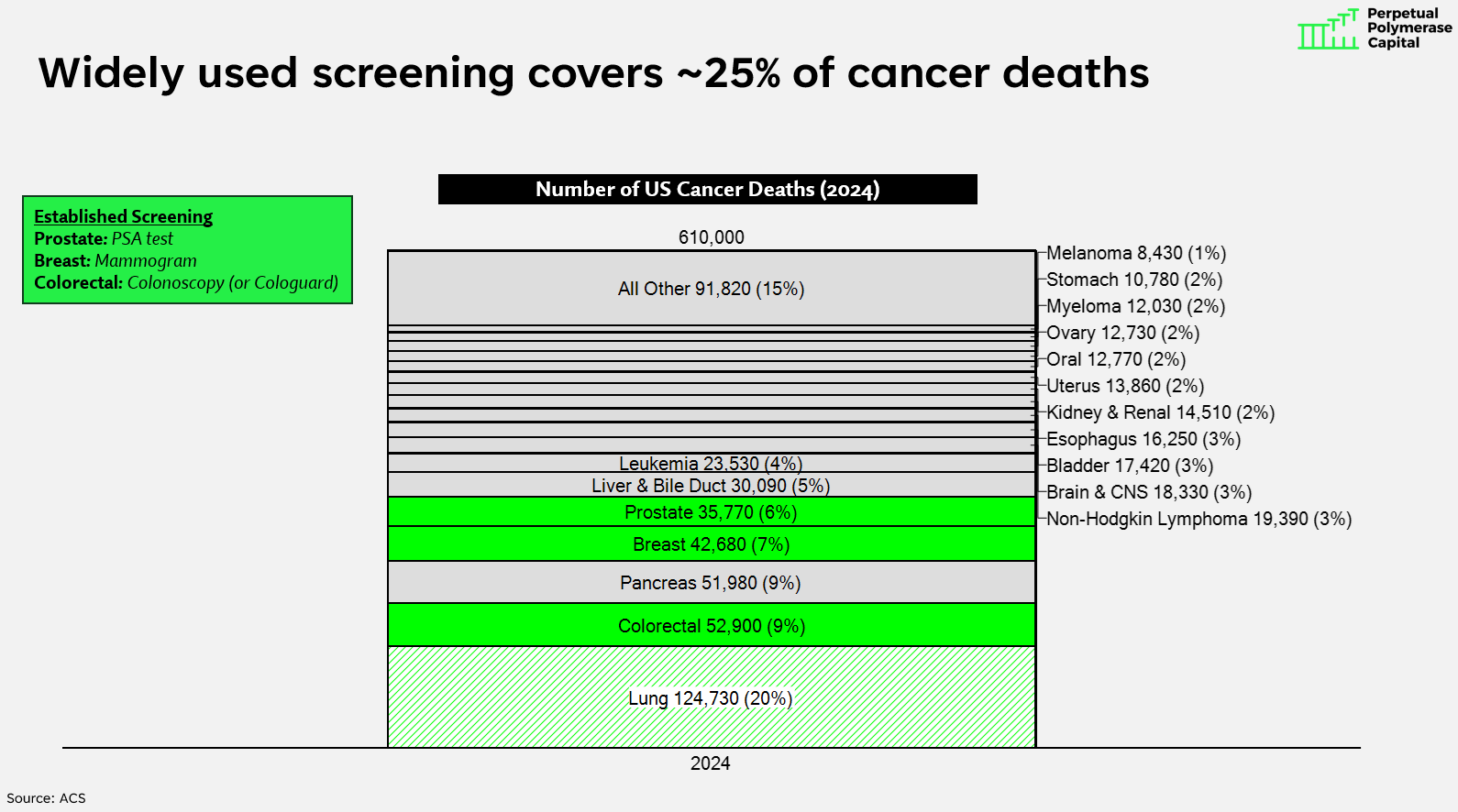

There are 3.1 million total deaths each year in the United States, of which cancer accounts for about 20% (~610K). This puts cancer behind only heart disease for lethality.

Pithily, if we solve cancer, we’re 20% of the way to immortality1.

Chart: Leading causes of death in the U.S. (2023), per CDC

If we want to decrease cancer deaths, it’s ideal to catch it early, when it’s more amenable to treatment.

Take lung cancer as an example. If diagnosed while still localized in the lung, the likelihood of surviving at least 5 years is 65%. If diagnosed after it has expanded regionally, to nearby lymph nodes, survival drops to 37%. Finally, if diagnosed after it has metastasized to distant organs, likelihood of surviving the subsequent 5 years is only 9% - less than one in ten.

The same pattern is recapitulated across cancer types.

Chart: 5-year survival rates for key cancers, based on stage at initial diagnosis

Catching cancer early is highly dependent on how obvious the symptoms are. Some cancers, like breast and testicular, often create noticeable lumps. This can tip the scales towards early detection. 65% and 60% of breast and testicular cancers are caught when they’re still localized, respectively.

Other cancers have fewer superficial signs - pancreas and lung being the two notorious examples. Only 18% of pancreatic cancers and 30% of lung cancers are caught when localized2.

Thus, there’s a need for broad-based screening programs than can detect all different types of cancer. However, of the major cancers, only three have widely-used screening today:

Colorectal - colonoscopy (or Cologuard stool test)

Breast - mammogram

Prostate - PSA test

Together, these three cancers account for about 130K cancer deaths per year, 25% of the 610K total. For the other 75%, we don’t have widely-used screening protocols3. Lung cancer - the biggest killer - does have a screening protocol (low dose CT scan for former smokers over age 50), but compliance is quite low.

Chart: U.S. cancer deaths by cancer type (2024)

Ideally, we’d have a generalized cancer screening test - one that detects many cancers in one fell swoop.

Enter MCEDs. These tests use DNA sequencing to find trace quantities of cancer DNA in the bloodstream. This requires a lot of sequencing horsepower - cancer cell DNA represents a small fraction of all DNA molecules found in the bloodstream, most of which are generated from normal physiological processes like white blood cell death.

MCEDs are emerging now because Illumina has driven the cost of sequencing down 50x over the last 15 years. $10,000 worth of sequencing in 2010 now costs $200. It’s economically feasible to do deep sequencing to find cancer DNA in the bloodstream. This is the core technological change that enabled the MCED market4.

This description makes MCEDs seem straightforward. They’re anything but.

As a general rule, advanced cancers (e.g., Stage 3 and 4) shed more DNA than early stage cancers - they have a higher “tumor fraction” in the bloodstream.

This makes MCEDs good at detecting late-stage cancers, but worse at detecting early-stage cancers, which is the type we really want to detect, since we can intervene early and change the course of disease.

The performance metrics from leading players in the space, like Guardant’s Shield colorectal cancer test and GRAIL’s multi-cancer Galleri test, lay bare the challenges. Both are poor at detecting early-stage cancers, with accuracy increasing as cancer progresses5.

Chart: Guardant & GRAIL sensitivity by stage of cancer

There are also differences in accuracy between cancers. Cancers that are highly vascularized and shed a lot of DNA are easy to detect. Those that do not are more difficult.

Thus, MCEDs struggle to detect early-stage cancer, and can have variable performance across cancer types6. But isn’t the fact that they detect some cancers better than nothing?

It’s complicated. Because these are screening tests (to be deployed in a large population of healthy people), it’s critical to limit false positives.

False positives are problematic because they generate additional medical work that could harm the patient.

Perhaps an MCED test that says you have lung cancer, and you get a CT scan, followed by a lung biopsy. Lung biopsies can occasionally cause complications like pneumothorax, hemorrhage, etc. Thus, limiting false positives is critical for designing a test that ultimately does more good than harm.

There is still a vigorous debate about whether the benefits of MCEDs outweigh the costs. That said, I expect MCEDs to continue to march forward despite these debates.

The Economics of MCED Tests

Major diagnostics companies see a big opportunity in the MCED market, and are racing to develop tests. Is their optimism justified?

To analyze the economics of MCED, we need to understand two factors:

Addressable market (TAM): Is it a big opportunity?

Unit economics: Is it a profitable opportunity?

The former is easy. The addressable market is huge. Assuming one test per year for the >100M Americans over 50 years old, at $500 per test, that’s a $50B TAM.

I think this is too optimistic, but the beauty of starting with $50B is that you can haircut it in many ways, and it’s still big. If the test is recommended once every 3 years (rather than every year), that’s a $17B annual TAM, the largest in diagnostics.

While the revenue TAM is huge, I am less sanguine on the profit TAM, which will ultimately drive value. I expect unit economics to be extremely challenging for MCED tests.

Three variables are critical:

What is the gross profit per test?

How many tests will each prescriber order per year? (e.g., what is the “gross profit opportunity per prescriber”)

What is the sales, marketing, and customer support spend required to service each prescriber?

If each physician generates high gross profit and can be serviced relatively cheaply, this is a recipe for excellent unit economics.

On the other hand, if each physician produces low gross profit, and requires a lot of sales & customer service effort, unit economics will be challenged.

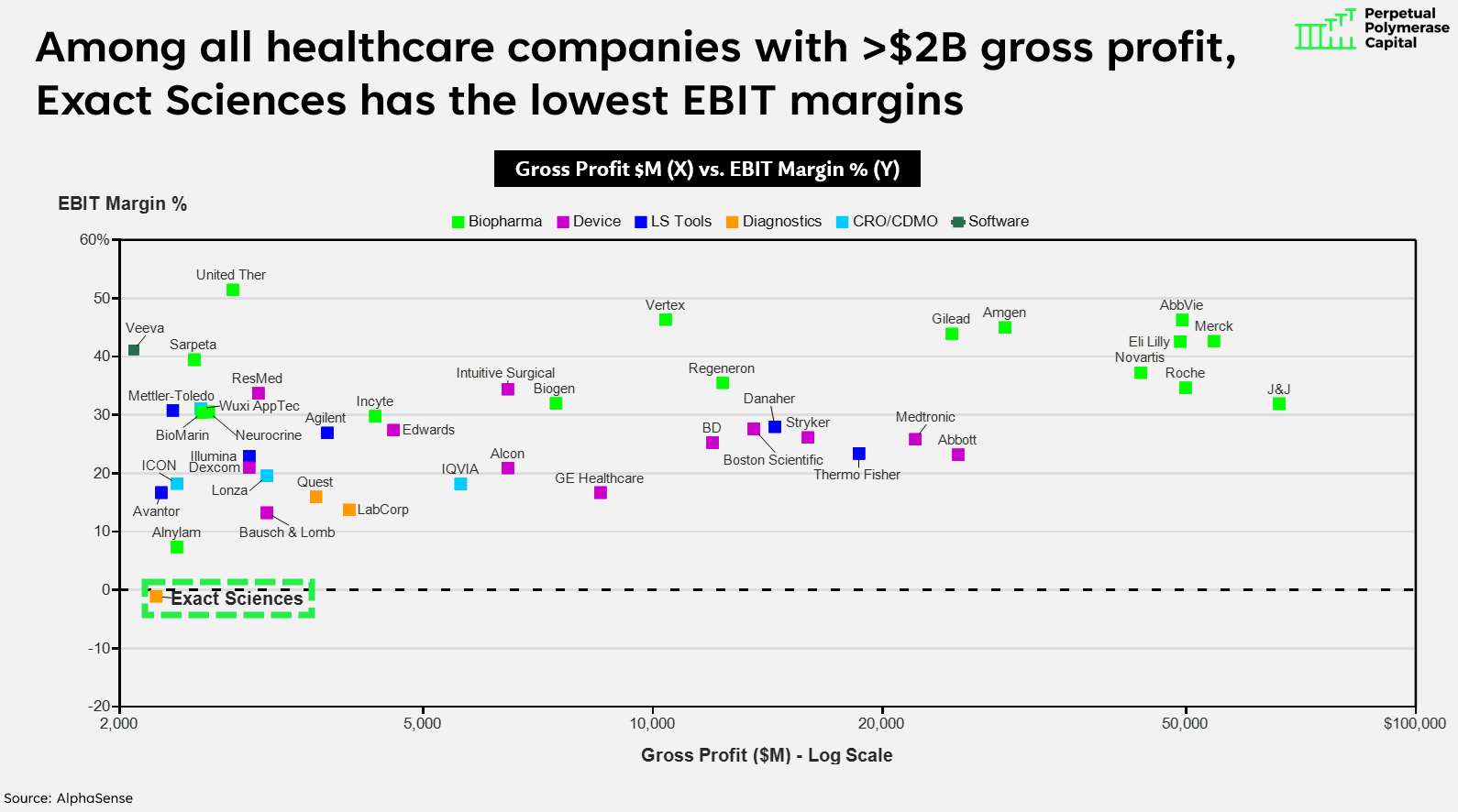

Before we dive in, let’s benchmark against Cologuard, since it is also a cancer screening test (specifically for colorectal cancer) prescribed by primary care physicians.

While Cologuard does over $2B revenue per year for its maker, Exact Sciences, it is not yet especially profitable7.

Indeed, among all companies in my healthcare coverage universe that produce more than $2B gross profit, Exact8 has the single worst margin profile:

Chart: EBIT margin percentage for healthcare companies >$2B gross profit in 2025

Exact’s difficulty turning a profit implies that selling diagnostics through the primary care channel is a difficult endeavor.

Let’s look at how MCEDs compare.

Gross Profit per Test

I expect MCED gross profit per test to be slightly lower than Cologuard.

Cologuard averages ~$600 reimbursement and requires ~$125 COGS, yielding ~$475 gross profit per test (79% gross margins).

A recently proposed Congressional bill seeks to set MCED pricing equal to Cologuard, thus ~$600. To be clear, this bill hasn’t become law. But, $600 is a reasonable assumption for long-term MCED pricing. Guardant currently achieves $600-700 ASP for Shield ($1,500 from Medicare, and $0 from private payers).

Over time, private payers should reimburse (they usually do so after the test achieves inclusion in guidelines such as ACS or USPSTF), but Medicare pricing will come down. Guardant has guided to $500+ ASP for Shield over the long term.

On the COGS side, MCED tests cost more to run than Cologuard. Compared to Cologuard’s $125, GRAIL and Guardant incur $450-500 worth of costs to run their Galleri and Shield tests, respectively.

The reason is that Cologuard does not require Illumina sequencing (it only looks for a small handful of DNA changes), while MCED looks for many DNA changes, and thus requires Illumina spend of $100-150 per test.

The rest of the COGS goes towards human labor (lab techs), other reagents and consumables (extraction; library prep), as well as fixed costs like facilities.

There will be some economies of scale here. Guardant has set a target of $200 COGS per test at scale. That said, a fair amount of COGS is labor (lab technicians that receive tubes of blood, extract DNA, and prepare it for the sequencer). While some of this could be automated, it’s not an obvious place for economies of scale.

All taken together, I expect MCED tests to achieve $400 gross profit per test, at 67% gross margin ($600 revenue and $200 COGS) - slightly lower than Cologuard.

Gross Profit Opportunity per Prescriber

We’ve established an expectation for gross profit per test. But to understand the unit economics, we must also assess how many tests a prescriber will order annually.

Here, I could see MCED tests being favorable to Cologuard.

Optimistically, the annual test TAM for Cologuard is 20M9. Given ~400,000 PCPs and PCP nurse practitioners in the US10, this equates to 50 tests and $23,750 annual “gross profit opportunity” per prescriber (50 tests * $475 gross profit per test).

This is low. Let’s compare it to an obviously excellent business, Eli Lilly’s tirzepatide, a GLP-1 drug mostly prescribed by PCPs. The average PCP has 300 patients that qualify for tirzepatide (obesity, diabetes, sleep apnea), and tirzepatide will produce $4,000 gross profit per patient ($5,000 revenue per patient * 80% gross margins). Tirzepatide’s gross profit opportunity per prescriber is $1.2M, 51 times higher than Cologuard.

How about MCED?

If we assume that all Americans over 45 should get an MCED test every 3 years, this implies a 40M annual test opportunity, thus, 100 tests per prescriber per year. At $400 gross profit per test, this yields a $40,000 gross profit opportunity per prescriber: almost double that of Cologuard, but still much closer to Cologuard than tirzepatide.

Sales & Marketing Costs

Now that we understand gross profit potential per prescriber, let’s evaluate the sales & marketing efficiency.

Exact spent $900M on sales & marketing in 2024, with a primary care salesforce of >1,000 reps. Thus, ~$800K fully loaded sales & marketing costs per sales rep. This is inclusive of sales rep compensation, but also all marketing, customer service, sales support, etc.

Using this assumption for sales & marketing costs per rep, we can fully evaluate the unit economics.

Each MCED prescriber has the potential to generate $40,000 gross profit per year, if TAM penetration is 100%. But TAM penetration never reaches 100%. Cologuard has been on the market for a decade and is 20% penetrated. At a more realistic 30% TAM penetration, the average MCED prescriber will do $12,000 gross profit per year.

Given $800K in annual costs per sales rep, this means each rep needs to cover 67 prescribers just to break even ($800K/ $12,000).

This is better than Cologuard (112 prescribers), but both are very challenging.

Again, compare to tirzepatide. Even if we assume Lilly has much lower TAM penetration (10%), they generate $120K gross profit per prescriber, needing only 7 prescribers to break even on $800K S&M spend. At 30% TAM penetration, Lilly breaks even on 2 prescribers.

If you need a one-line explanation for why Lilly has 40% EBIT margins and Exact Sciences has 0%, it’s this.

Table: Unit economics for MCED tests vs. Cologuard vs. tirzepatide

In order for diagnostics companies to generate healthy economics, two things need to be true: TAM penetration needs to be relatively high (>20%), and each sales rep needs to cover a lot of physicians - 250+ per rep11.

The X-Factor: Competition

There’s one more major factor to consider, which will have a critical impact on MCED profitability: competition.

One of the reasons Cologuard’s economics just barely work is because it is effectively a monopoly - historically, there have been no actively marketed competitors in the colorectal cancer screening space.

If we assume Cologuard had a competitor and each had 50% market share, then instead of 112 prescribers required to break even, each company would need 224 prescribers to do so. This is unworkable.

Thus, the competitive landscape will be key to determining MCED profitability. If, like Cologuard, one winner emerges, I expect modest profitability (perhaps 15-20% operating margin at maturity for the winner). If there are 2-3 companies marketing MCED tests with relatively equivalent market shares, it’s hard for me to see this as as profitable category for the foreseeable future.

The table below shows the number of prescribers required to break even on a sales rep at various levels of market share. At lower market share, the required prescriber count becomes unrealistically high.

Table: Unit economics for MCED tests in various market share scenarios

Conclusion

Early cancer detection testing is fast becoming a clinical reality.

My expectation is that MCED will become a large revenue category, but one that struggles to generate profits, especially if there are 2-3 companies actively marketing similar tests. This is how it appears right now - GRAIL, Guardant, Exact, and Natera are all running at the opportunity, with none obviously possessing a superior test.

What could we be missing? If the market does end up being very profitable, what did we get wrong?

There’s a chance I’m underestimating the annual volume opportunity. Perhaps guidelines will recommend once per year screening. If this happens, then the TAM is 120M tests per year, rather than 40M. Gross profit per prescriber opportunity triples. At $120K gross profit opportunity per year, the economics work better than $40K.

Perhaps ASP also comes in higher. If ASP per test is $800, using the same $200 COGS, this yields $600 gross profit per test.

If both of these things happen - screening once per year, and $600 gross profit per test, then each prescriber’s annual gross profit opportunity jumps to $180,000. At 30% TAM penetration, we only need 15 prescribers to break even. Now we’re cooking with gas.

The other areas are harder for me to see significant upside. Could COGS be lower than $200? We’re a long way away from that today, so I’d be surprised.

How about salesforce efficiency? Could each rep cover 600 physicians instead of 300? This also seems difficult. Exact tried to curtail S&M spend for Cologuard over the last few years, and growth slowed meaningfully. Screening tests like Cologuard (and MCED) are “promotionally sensitive” - they require a lot of sales effort to convince physicians to prescribe.

Is there a way to cut the prescriber out of the loop, so the test is marketed to consumers rather than prescribed by physicians? Imagine a “Hims” like experience where an online doctor writes a prescription after you fill out a brief questionnaire, and then you go to LabCorp or Quest to get blood drawn. This is interesting and provocative, and could be a way to change the equation. I’d love to see a company try this, but I’m not sure consumers are health-conscious enough to partake.

In summary, primary care is an extremely difficult segment to sell into, given the vast number of providers. To build a profitable business, it’s critical to have high gross profit per prescriber. While some drugs with high prices and wide indications (like tirzepatide) achieve this, diagnostics have struggled to do so.

I’m optimistic about the clinical benefits of MCED tests. That said, their profitability remains an open question.

Why isn’t eliminating heart disease deaths as charismatic as eliminating cancer? There’s something more emotionally resonant about cancer. It’s an interesting sociological thing.

There is a fascinating statistical literature on whether early diagnosis actually improves survival or whether the observed difference is mostly a function of lead-time bias. Suppose I catch a cancer while it’s Stage I, and it’s going to kill me in exactly 6 years, no matter what. Or suppose I catch that exact same cancer 5 years later (when it’s Stage IV) and it’s going to kill me in 1 year. There’s nothing fundamentally different between these cancers - I will die on the same calendar date. But the first case “looks” to have much better 5 year survival.

Cervical cancer also has a well-established screening regimen, with HPV tests and pap smears. But, cervical cancer accounts for <1% of annual US cancer deaths (~4,300)

Exponentials are amazing - both Moore’s Law and Flatley’s Law (sequencing getting cheaper over time) consistently open up new markets that were wildly implausible only years before.

Shield has been controversial since its landmark trial results were published two years ago. Judged from a test accuracy perspective, it’s clearly worse than colonoscopy or Cologuard. Cologuard detects 87% of Stage I cancers, compared to Shield’s 55%. Likewise, Cologuard detects 45% of advanced adenomas, compared to Shield’s 13%.

But at the same time, Shield is more convenient than either Cologuard or colonoscopy. In an ideal world, everyone would do colonoscopy or Cologuard. And if they refused to do that, they’d use Shield.

In reality, some people will probably do Shield instead of the other options, which is suboptimal.

Despite the controversy, Shield earned FDA approval and is reimbursed by Medicare.

Can these tests get better at finding early stage cancers? My big question is whether improvement is mostly a matter of more sequencing, or whether the problem lies elsewhere. If these tests get more accurate if we throw more sequencing at them, that seems like a straightforward path to continuous improvement and higher uptake, since sequencing should continue to get cheaper. Based on my conversation with leaders in the field, I do not think more sequencing is the main bottleneck.

We explored the P&L profiles of diagnostics companies, including Exact, in a previous post.

EXAS sells tests other than Cologuard (e.g., OncotypeDx) but most of its revenue and spend is dedicated to Cologuard.

Doctors typically offer Cologuard to individuals who are not up to date with colonoscopy, of which there are 60M. At a once per three years test interval, that’s 20M per year. Cologuard currently does ~4.5M tests per year, so ~20% penetrated.

Bureau of Labor Statistics says there are 280K PCP physicians and another 280K primary care NPs, for 560K total. I assume that some of these are small enough not to warrant targeting, so use 400K as the target.

I’d love to compare “speeding tickets per sales rep” between Exact and Lilly. My guess is that Exact’s reps generate quite a few speeding tickets, as they race between doctor offices every day. Lilly’s reps, on other hand, can afford to drive slowly, go out to lunch, get a workout in, etc.

Hi Edward.

Thank you. Just catching up with the 4-5 most recent posts.

I was wondering if you have any thoughts on radio-pharmaceuticals, say copper-64 (Cu-64 or 64Cu) or other isotopes? That is imaging as an EARLY detection tool? Seems less invasive and potentially more scalable (mass market type of product)?

Thanks.

Question - does your calculation assume any given prescriber would split their orders across >1 provider, assuming competition? Or is it more likely that a prescriber would prefer one provider and send all their patients there? In the latter case, does that change the impact of competition? Would I just need to cover 67 prescribers as long as they are super loyal?